Swing Trading Taxes: Short-Term Capital Gains and Wash Sales

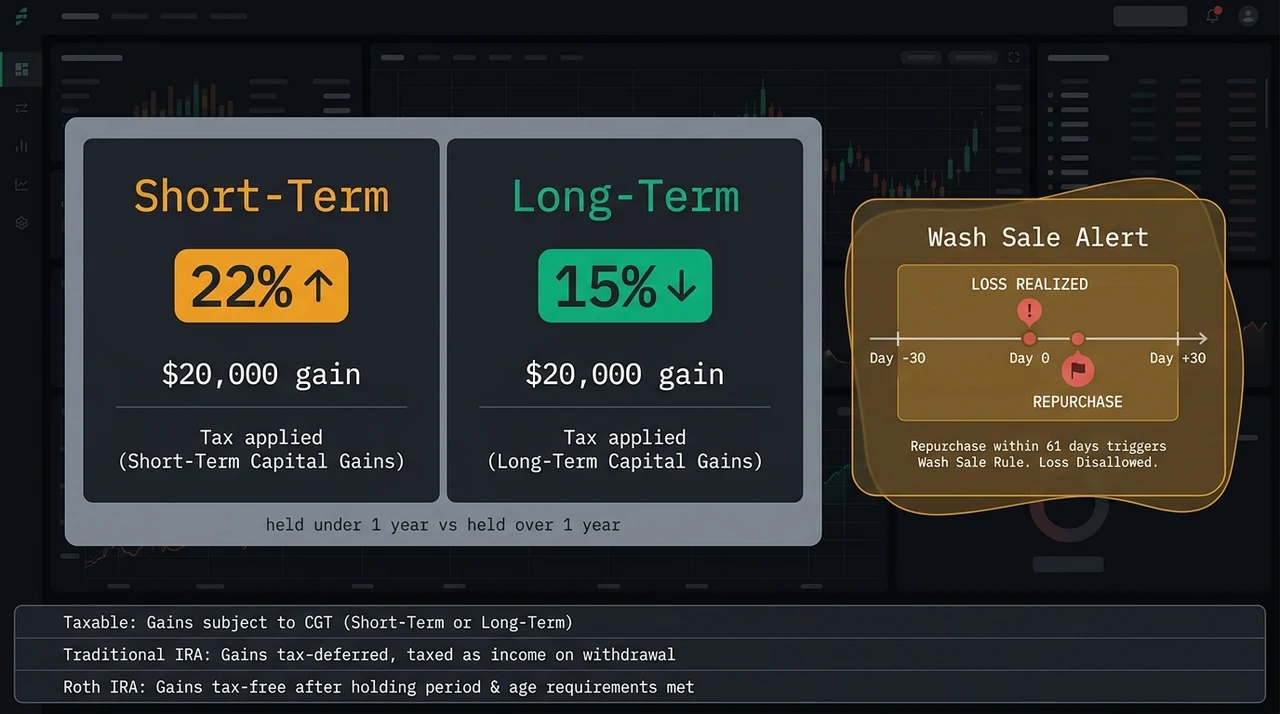

Short-term capital gains are taxed as ordinary income. For a swing trader in the 24% federal bracket who generates $50,000 in annual trading profits, that bracket means $12,000 in federal tax — versus $7,500 if the same gains qualified for long-term treatment at 15%, according to 2024 IRS rate schedules (Revenue Procedure 2023-34). The $4,500 annual difference, reinvested at the same return rate, compounds into roughly an additional year's worth of starting capital within a decade.

Most swing trading gains are short-term by design — holds of 2 to 30 days are taxed at ordinary income rates, not preferential capital gains rates. Tax planning is part of the edge. The mechanics are straightforward; the traps are where most active traders lose money.

How Swing Trading Profits Are Taxed

Sell within one year of purchase and the gain is short-term, taxed at ordinary income rates (10%–37% federally for 2024). Sell after holding more than one year and it qualifies for long-term treatment at 0%, 15%, or 20%. Most swing traders hold 2–30 days, so nearly all realized gains are short-term — taxed at the highest applicable rate.

The 2024 ordinary income brackets that govern short-term capital gains run from 10% at the lowest income levels to 37% above $609,350 for single filers. The table below shows the federal tax difference on the same $20,000 gain depending on holding period and total income:

| Annual Income (Single) | STCG Rate | Tax on $20k Gain | LTCG Rate | Tax on $20k Gain | Federal Tax Saved by Qualifying |

|---|---|---|---|---|---|

| $80,000 | 22% | $4,400 | 15% | $3,000 | $1,400 |

| $150,000 | 24% | $4,800 | 15% | $3,000 | $1,800 |

| $220,000 +NIIT | 35.8% | $7,160 | 18.8% | $3,760 | $3,400 |

| $400,000 +NIIT | 38.8% | $7,760 | 18.8% | $3,760 | $4,000 |

The holding period cutoff is the acquisition date to the sale date — the anniversary date itself is still short-term. A position opened June 15, 2024, becomes long-term only when sold on or after June 16, 2025. The precise calendar date matters for positions approaching the threshold in Q4.

For swing traders, this creates a specific decision point in the 30–60 day holding range. A position that is still technically a swing trade but has been working quietly for six to eight weeks may be worth holding past the one-year mark if the chart structure supports it. The tax math alone can justify the extended hold when gain size is material.

The Wash Sale Rule — The Most Expensive Tax Trap for Active Traders

The wash sale rule (IRC § 1091) disallows a realized loss if you purchase the same or substantially identical security within 30 days before or after the loss sale — a 61-day window total: 30 days before the sale, the day of sale, and 30 days after.

As IRS Publication 550 (Investment Income and Expenses, 2023 edition) states: "You cannot deduct losses from sales or trades of stock or securities in a wash sale …" The rule has been in effect since 1921, designed to prevent traders from realizing artificial tax losses while maintaining the same economic exposure.

The critical distinction: the disallowed loss is not gone permanently. It is added to the cost basis of the replacement security, effectively deferring the loss until you dispose of that replacement position outside the wash sale window. But if year-end arrives while you hold the replacement, the deferred loss carries into the next tax year — creating cost basis complexity that accumulates across periods.

Swing traders are particularly exposed because they rotate through the same setups repeatedly. A trader working 10–15 setups in rotation — managed through a swing trading watchlist — may execute the same stock three or four times per quarter, with each trade potentially inside the prior trade's 30-day window. These wash sale chains compound, and cost basis errors on year-end 1099-B statements are common.

Three specific scenarios to monitor:

Same stock within 30 days. The direct case. Realize a loss on Monday, rebuy the same ticker on the following Tuesday — 8 days later — and the loss is disallowed regardless of different price levels or a different broker account.

Options on the same stock. The IRS treats options as substantially identical to the underlying in most contexts. Selling a stock at a loss and buying a call option on the same stock within the 30-day window is generally a wash sale. Buying an out-of-the-money call to maintain exposure after a tax-loss sale does not cure the wash sale — it triggers it.

IRA purchases after a taxable-account loss. If you sell a stock at a loss in a taxable brokerage account and buy the same security in your IRA within 30 days, the wash sale rule applies — and the loss is permanently disallowed, not deferred. The IRA is a separate tax-exempt entity; the cost basis adjustment has nowhere to go. This is the worst-case wash sale outcome and a common error for traders who manage taxable and retirement accounts simultaneously.

The Net Investment Income Tax: The 3.8% Most Traders Miss

Single filers with modified adjusted gross income above $200,000 — and married filers above $250,000 — owe an additional 3.8% Net Investment Income Tax (NIIT) on investment income, including capital gains. This surcharge pushes the effective top federal rate on short-term capital gains to 40.8%, not 37%.

The NIIT was introduced by the Affordable Care Act and applies to net investment income above the income threshold. It is calculated separately from the regular income tax and does not affect which income bracket applies — it is a flat surcharge on the investment income component. For a trader generating $100,000 annually in trading profits at the top bracket, the NIIT alone represents $3,800 per year in additional federal tax.

The income threshold is not indexed for inflation. A trader whose combined income was just below $200,000 in prior years may cross the NIIT threshold as trading performance improves. State income taxes compound the picture further — California, New York, New Jersey, and Oregon apply full ordinary income rates to all capital gains with no preferential treatment for long-term.

Tax-Efficient Account Structures for Swing Traders

Trading inside a Roth IRA eliminates both ordinary income tax and the NIIT on qualifying distributions. Contributions are post-tax, but growth and qualifying distributions after age 59½ and a five-year holding period are entirely tax-free — including all realized trading gains from within the account. No short-term capital gains rate, no NIIT, no wash sale deferred adjustments to carry across years.

The 2024 Roth IRA contribution limit is $7,000 ($8,000 if 50 or older), which constrains position size but not the compounding advantage. The comparison across account types:

| Account Type | Tax Treatment on Gains | 2024 Contribution Limit | Best Use Case |

|---|---|---|---|

| Taxable brokerage | STCG at ordinary income; LTCG at 0/15/20% + NIIT if applicable | Unlimited | Large positions, full flexibility, tax-loss harvesting |

| Traditional IRA | Tax-deferred; all distributions taxed as ordinary income at retirement | $7,000 ($8,000 if 50+) | High-income trading years; lower-bracket retirement expectation |

| Roth IRA | Post-tax contributions; qualifying distributions permanently tax-free | $7,000 ($8,000 if 50+) | Long-term compounding; eliminating NIIT exposure permanently |

The wash sale trap in IRAs requires specific attention. Selling at a loss in a taxable account and buying the same security in your IRA within 30 days permanently disallows the loss on the taxable side — the cost basis adjustment has nowhere to go in a tax-exempt account. Never use an IRA purchase to reset the wash sale window on a taxable loss.

For traders with MAGI above the Roth IRA income phaseout ($146,000 single / $230,000 married for 2024), the backdoor Roth conversion provides an indirect path. This is specialized territory — the interaction between conversion accounting and wash sale chains across account types requires a CPA familiar with active trader returns.

Traditional IRAs defer rather than eliminate taxes. Gains compound tax-deferred, but every qualified distribution is taxed as ordinary income at the then-current rate. For traders currently in lower brackets expecting higher future income, this timing dynamic may work against them.

Estimated Taxes and Record-Keeping

Trading gains have no withholding mechanism. No broker withholds federal taxes from realized capital gains during the year — the full tax obligation accumulates until filing or until you make estimated quarterly payments. Traders who do not make quarterly estimated payments risk underpayment penalties from the IRS.

The IRS requires estimated payments from any taxpayer who expects to owe more than $1,000 in federal tax not covered by withholding. For 2024, due dates are April 15 (Q1), June 17 (Q2), September 16 (Q3), and January 15, 2025 (Q4). The prior-year safe harbor — paying 100% of the prior year's total tax liability, or 110% if AGI exceeded $150,000 — avoids underpayment penalties regardless of current-year actual liability.

Precise trade records are the foundation of accurate tax reporting and the defense against audit exposure. The IRS requires specific lot identification for taxpayers who want to control which shares they are selling — without it, FIFO (first in, first out) applies by default, which may increase taxable gains in multi-lot situations. Required documentation for active traders:

- Open and close dates for every position

- Entry and exit prices

- Number of shares per trade

- Wash sale flags and adjusted cost basis for losing trades

- Year-end cost basis statements and 1099-B from the broker

Mark-to-market accounting (IRC § 475(f)), elected by traders who qualify as "traders in securities" under IRS standards, eliminates wash sale complications entirely — all positions are treated as sold at year-end fair market value, and all gains and losses are ordinary income or loss (not capital). This election must be made before the start of the tax year and requires meeting specific trading activity tests. It is not appropriate for part-time traders. Consult a CPA or enrolled agent familiar with active trading returns before exploring it.

EasySwing.trading's journal logs every trade with open date, close date, and gross P&L — a timestamped record for holding period calculation and cost basis tracking. For the income math that downstream tax planning is built on, see swing trading income: the math behind sustainable returns and position sizing with R-multiples.

Tax Checklist for Swing Traders

- ✅Track every trade with open date, close date, entry and exit price, and shares — the IRS requires this for specific lot identification

- ✅Make quarterly estimated tax payments if trading income is not covered by withholding (April 15, June 17, September 16, January 15)

- ✅Verify wash sale adjustments on your broker's year-end 1099-B — errors are frequent, particularly across taxable and IRA accounts

- ✅Consider holding profitable positions past the one-year mark when the chart structure supports it and the gain is material

- ✅Consult a CPA annually — wash sale chains, NIIT thresholds, and estimated tax safe harbors require professional review

- ❌Do not rebuy the same stock within 30 days of a loss sale — the wash sale rule disallows the deduction and adds complexity to cost basis tracking

- ❌Do not buy the same security in your IRA after a taxable-account loss — the loss is permanently disallowed on the taxable side in that scenario

- ❌Do not count the anniversary date as long-term — a position opened June 15, 2024, is short-term if sold on June 15, 2025; it becomes long-term only on June 16, 2025

- ❌Do not wait until December to address wash sale chains — multiple months of rotations in the same tickers compound the adjustments and are harder to unwind late in the year

- ❌Do not assume your broker caught all wash sales — cross-check especially if you trade the same tickers in both a taxable account and an IRA simultaneously

EasySwing.trading automatically logs swing trade entries, exits, and holding periods in the trade journal, giving you a complete timestamped record for holding period classification and cost basis reporting. For the after-tax income math behind sustainable trading, see swing trading income: the math behind sustainable returns. For the position sizing framework that keeps losses manageable before the tax year closes. This post is educational content — not tax advice. Consult a qualified CPA or enrolled agent for personalized guidance. Scan results are for informational purposes only. See our Risk Disclaimer.

Frequently Asked Questions

Are swing trading profits taxed as capital gains?

Yes. Swing trading profits are capital gains, but the rate depends entirely on the holding period. Gains from positions held one year or less are short-term capital gains, taxed at ordinary income rates (10%–37% federally for 2024). Gains held longer than one year qualify for long-term capital gains rates (0%, 15%, or 20%). Because most swing traders hold 2–30 days, nearly all gains are short-term.

What is the tax rate on short-term trading profits?

Short-term capital gains are taxed at your ordinary income rate — the same bracket that applies to wages and salaries. For 2024, federal brackets run from 10% at the lowest income levels to 37% above $609,350 for single filers. Taxpayers with modified AGI above $200,000 (single) or $250,000 (married) also owe the 3.8% Net Investment Income Tax, bringing the effective top federal rate to 40.8%.

How does the wash sale rule affect swing traders?

The wash sale rule (IRC § 1091) disallows a loss deduction if you buy the same or substantially identical security within 30 days before or after the loss sale — a 61-day window total. The disallowed loss is not gone permanently; it is added to the cost basis of the replacement position, deferring it to a future sale. Swing traders who rotate in and out of the same setups trigger this rule frequently, creating complex lot-tracking requirements.

Can I swing trade inside a Roth IRA?

Yes. Trading within a Roth IRA is legal and generates no taxable events on gains as long as you avoid prohibited transactions. Qualifying distributions after age 59½ and a five-year holding period are entirely tax-free — including all realized trading gains from within the account. The 2024 contribution limit is $7,000 ($8,000 if 50 or older). One critical trap: selling at a loss in a taxable account and buying the same security in your IRA within 30 days permanently disallows the taxable loss.

Do I need to pay estimated taxes on swing trading gains?

Yes, if you expect to owe more than $1,000 in federal tax not covered by withholding. Brokers do not withhold taxes on realized trading gains. The IRS requires quarterly estimated payments (due April 15, June 17, September 16, January 15) from taxpayers above the $1,000 threshold. Use the prior-year safe harbor — pay 100% of last year's total tax liability, or 110% if AGI exceeded $150,000 — to avoid underpayment penalties regardless of current-year income.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. EasySwing is a stock screening tool, not a registered investment advisor. All trading involves risk. Read our full disclaimer →